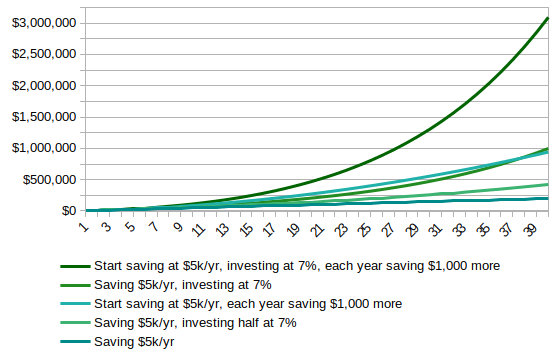

There is often a hard held belief that no matter what, you should always buy the place you live in, because after all when you rent you just throw money out of the window or rather to your landlord that you’ll never see again. While when buying a home, you always pay part of the mortgage towards the principal so you increase your equity, so you increase your assets.

Buying vs Renting a Home

Housing Is Your Biggest Expense

For most households, the money spent on the place we live in is the number one budget, taking roughly 30% of the annual expenses. It’s therefore extremely important to spend wisely on housing and it’s often where a lot of money can be saved.

As seen here, regardless of whether you are buying or renting, the place you live in is never an asset and always is a liability, short of house hacking (more on that in another post). A home takes money out of your pocket, so it’s a liability from a cash flow perspective.

That said, while the place you live in is always a liability, the game is to reduce such liability, to save as much money as you can.

And in reality the answer to the buying vs renting argument, is always: it depends.

It depends how much the home cost versus how much you would pay to rent a similar home.

Let’s look at the usual associated costs in each case:

Renting Costs

The renting costs are usually straightforward: the rent you pay to your landlord.

Buying Costs

When buying a home, there are several expenses associated with owning a home also known as unrecoverable costs:

- The closing costs when buying a home

- The mortgage payment

- The home insurance

- The property taxes

- Miscellaneous maintenance expenses

So to figure out whether you should buy or rent you need to figure out if the buying costs or higher or lower than what it would cost to rent a similar home in the same area, for the time period you expect to live there.

There are plenty of calculators out there to help you estimate whether you should buy or rent, but the rule of thumb is: if in your area real estate is very expensive (e.g. the San Francisco Bay Area circa 2020 where a 1200 sq. ft home is worth +$1,000,000), it will usually be more advantageous to rent. Conversely if real estate is much cheaper (e.g. in Memphis, TN circa 2020 where a 1200 sq. ft home is usually worth around $90,000), it will usually be more advantageous to buy.

Now there are always exceptions: you may be able to find a cheap house in an expensive area or find an extremely cheap rental in an area where real estate is cheap. That’s why you should always run the numbers, but hopefully that gives you the feel and the basics on how you should allocate your housing costs, which is for most households the biggest budget expense.

The 5% Rule

If you want a quick and easy rule of thumb to figure out whether you should buy or rent, Benjamin Felix at PWL Capital came up with the 5% rule, which estimates that homeowners usually spend 5% of the house price annually, between taxes, maintenance, opportunity cost.

Therefore if the annual rent is less than 5% of what the house would cost, it’s usually preferable to rent.

If the annual rent is more than 5% of what the house would cost, it’s usually preferable to buy.

For example, let’s take a house that would cost $100,000 and the monthly rent is $700. The 5% rule says, the rent should not be more than 5% x $100,000 = $5,000 annually. The rent annually is: 12 x $700 = $8,400. Hence in this case it would be interesting to buy the house rather than renting, according to the 5% rule.

Now let’s take a house that would cost $1,000,000 and the monthly rent is $3,000. The 5% rule says, the rent should not be more than 5% x $1,000,000 = $50,000 annually. The rent annually is: 12 x $3,000 = $36,000. Hence in this case it would be interesting to rent the house rather than buying, according to the 5% rule.

Of course the 5% rule is an oversimplification and it’s just a quick guideline to get a back of the envelope estimate. As mentioned above it’s important to get the actual numbers (as taxes may be different based on where you live, the financing cost may be different…) to have a more accurate estimate on whether it’s financially more advantageous to buy or rent.