“The Automatic Millionaire” by David Bach is not just a book; it’s a roadmap to financial freedom. In this summary, we’ll explore the key principles outlined by Bach, focusing on the power of automation in building substantial wealth effortlessly.

The Automatic Millionaire by David Bach Summary

The Essence of Automatic Wealth Creation

At the heart of Bach’s philosophy lies the concept of “automatic wealth creation,” a systematic approach to saving and investing that eliminates the need for willpower and decision-making. By automating financial processes, individuals can effortlessly accumulate wealth over time, even on modest incomes.

The Automatic Millionaire outlines a simple yet powerful four-step plan to achieve financial freedom:

Pay Yourself First: Prioritize saving by automatically transferring a portion of your income into savings or investment accounts before you even see it.

Set Up Automatic Investments: Schedule regular contributions to your investment portfolio, ensuring consistent growth and compounding of your wealth.

Increase Your Income: Explore opportunities to increase your earning potential, whether through career advancement, side hustles, or investments.

Protect Your Wealth: Safeguard your financial future by obtaining adequate insurance coverage and establishing sound financial planning practices.

The Power of Automatic Savings

In the world of financial success, small consistent actions can lead to significant results. Bach emphasizes the importance of setting up automatic savings. Whether it’s through employer-sponsored retirement plans or automated transfers to a savings account, the act of automating savings ensures a disciplined approach to wealth-building.

Make Your Home an Automatic Money Machine

Bach introduces the concept of the “Homeownership Automatic Millionaire.” By leveraging the power of real estate, individuals can transform their homes into financial assets. This section explores tips on how to make homeownership a key element in your journey to financial success.

Debt Reduction Strategies

Debt can be a major roadblock on the path to wealth. Bach provides insights into automating debt payments, allowing individuals to gradually free themselves from financial burdens. The ripple effect of reducing debt contributes significantly to overall financial freedom.

Automate Your Investments for Long-Term Wealth

Investing doesn’t have to be complex. Bach’s principles emphasize automated investment strategies, allowing individuals to benefit from compounding returns over time. This section delves into the specifics of his approach and how it can lead to long-term wealth.

The Latte Factor and Small Changes

In one of Bach’s most famous concepts, the “Latte Factor,” he highlights the impact of small, daily expenses on long-term finances. This section encourages readers to identify and modify these habits, redirecting funds toward automatic savings and investments.

Bach introduces the concept of the “Latte Factor,” highlighting the transformative power of small, consistent actions. By eliminating unnecessary expenses, such as daily latte purchases, and redirecting those funds towards savings or investments, individuals can accumulate significant wealth over time. This principle underscores the importance of mindful spending and the ability to make small sacrifices for long-term gains.

The Power of Compound Interest: Exponential Growth

The Automatic Millionaire emphasizes the remarkable impact of compound interest, the phenomenon where your earnings generate additional earnings over time. By starting early and investing consistently, individuals can harness the power of compound interest to achieve exponential wealth growth.

Achieving Financial Independence: A Personalized Journey

Bach recognizes that financial independence is a unique journey for each individual, shaped by personal circumstances, goals, and risk tolerance. He encourages readers to develop a personalized financial plan tailored to their specific needs and aspirations.

Automatic Millionaire Retirement Plan

Retirement planning can seem daunting, but Bach simplifies it through automation. By consistently contributing to retirement accounts, individuals can secure a comfortable and worry-free retirement. This section provides a step-by-step guide to creating an automatic millionaire retirement plan.

Building an Emergency Fund Automatically

Financial peace of mind comes from having a robust emergency fund. Bach’s approach to automatic emergency savings ensures that unexpected expenses don’t derail your financial journey. Learn how to build and maintain a safety net effortlessly.

The Automatic Millionaire Mindset

Becoming an automatic millionaire isn’t just about actions; it’s a mindset shift. This section explores the habits and attitudes that contribute to financial success, emphasizing the role of consistency and determination.

Overcoming Financial Obstacles: Conquering Fears and Debts

The book acknowledges the challenges and fears that often hinder financial progress. Bach provides strategies for overcoming these obstacles, including debt elimination techniques and mindset shifts to embrace financial responsibility.

Overcoming Challenges

While the concept of automatic wealth-building is powerful, it’s not without challenges. This section addresses common obstacles and provides practical tips for overcoming them. Stay motivated on your path to financial freedom.

Teaching Kids the Automatic Millionaire Way

Financial education is key, even from a young age. Discover the importance of teaching kids about money and how to instill automatic saving habits early on. Lay the foundation for their future financial success.

Automate Your Taxes

Tax season can be stressful, but Bach offers insights into simplifying the process. Discover how to maximize tax benefits through automated strategies, ensuring you keep more of your hard-earned money.

Adapting the Automatic Millionaire Principles

Bach’s principles are versatile and can be adapted to various financial goals. This section guides readers on customizing the automatic millionaire approach to fit individual circumstances, ensuring practical application.

The Automatic Millionaire’s Enduring Legacy

The Automatic Millionaire has transformed the lives of countless individuals, empowering them to take control of their finances and achieve their dreams of financial freedom. Its simple yet effective strategies have inspired millions to embrace automation, prioritize saving, and cultivate wealth-building habits.

David Bach’s The Automatic Millionaire stands as a testament to the power of financial literacy and the transformative impact of automation. By providing practical guidance and inspiring stories, the book has empowered countless individuals to take charge of their finances, achieve their financial goals, and secure their futures.

Conclusion

In conclusion, “The Automatic Millionaire” isn’t just a book; it’s a blueprint for financial success. By embracing the power of automation in savings, investments, and everyday financial habits, anyone can pave the way to becoming an automatic millionaire.

FAQs

Is “The Automatic Millionaire” suitable for beginners in finance?

Absolutely! David Bach’s writing style and practical advice make it accessible to individuals at all levels of financial knowledge.

How soon can I expect to see results by following the automatic millionaire principles?

Results vary, but many individuals notice positive changes in their financial situation within a few months of implementing these strategies.

Can I still become an automatic millionaire if I have existing debts?

Yes, Bach provides strategies for automating debt repayment, helping individuals gradually eliminate their debts.

Are the investment strategies mentioned in the book applicable to different risk tolerances?

Yes, Bach’s investment principles can be tailored to accommodate varying risk tolerances and financial goals.

Is it necessary to own a home to benefit from the concepts in the book?

While homeownership is discussed, many of Bach’s principles can be applied by individuals who do not own homes.

In the realm of real estate, enhancing the appeal and functionality of rental properties is a strategic move for landlords looking to attract quality tenants and maximize their investment returns. One of the most impactful ways to achieve this is through a well-thought-out kitchen remodel. This article will delve into the various factors influencing the cost of remodeling a rental property’s kitchen, providing insights into budgeting strategies, essential components, and the potential return on investment.

Factors Influencing Kitchen Remodel Costs

Property Location and Market Trends

The geographical location of a rental property significantly impacts the cost of a kitchen remodel. In high-demand markets, where property values are on the rise, costs for materials and labor tend to be higher. Being aware of local market trends is crucial for budgeting effectively.

Kitchen Size and Layout Considerations

The size and layout of the kitchen play a pivotal role in determining remodeling costs. Larger kitchens naturally require more materials, and intricate layouts may involve additional labor expenses. Understanding the specifics of the property’s kitchen is essential for accurate cost estimates.

Quality of Materials Used

The choice of materials can make or break a remodeling budget. Opting for high-quality, durable materials may incur higher upfront costs but can result in long-term savings by reducing maintenance and replacement expenses. Striking the right balance is key.

Labor Costs and Contractor Selection

Labor costs constitute a significant portion of a kitchen remodel budget. Choosing between hiring professionals and a do-it-yourself approach requires careful consideration. Quality contractors may have higher upfront costs but can deliver a more polished and efficient result.

Budgeting Strategies

Allocating Funds Efficiently

An effective budget allocates funds to areas that yield the most impact. Prioritizing critical components such as cabinetry, countertops, and appliances ensures that the essentials are addressed before allocating funds to less critical aspects.

Identifying Cost-Saving Opportunities

Cost-saving opportunities abound in kitchen remodeling. From exploring discounts on materials to considering gently used appliances, savvy landlords can find ways to reduce costs without compromising quality.

Prioritizing Essential Renovations

Not all kitchen renovations are created equal. Focusing on essential improvements that enhance functionality and aesthetics can prevent unnecessary expenditures on non-essential features.

Essential Components of a Kitchen Remodel

Cabinetry and Storage Solutions

Cabinetry is a focal point in any kitchen. Choosing durable and aesthetically pleasing cabinets not only enhances the visual appeal but also contributes to efficient storage solutions, a key consideration for potential tenants.

Countertops and Backsplash Options

Countertops and backsplashes are elements that combine functionality with design. Exploring cost-effective yet visually appealing options can significantly impact the overall budget.

Appliances and Their Impact on the Budget

The choice of appliances can range from budget-friendly to high-end. Assessing the needs of potential tenants and balancing quality with cost is crucial for an economically sound remodel.

Flooring Choices for Durability and Aesthetics

Flooring is a foundational aspect of any kitchen remodel. Durable materials that withstand high traffic and spills are essential for longevity and tenant satisfaction.

Average Costs for Kitchen Remodel Components

A kitchen remodel is an exciting project that can transform the heart of your home and significantly enhance its value. However, it’s important to be aware of the associated costs to ensure the project aligns with your financial goals and expectations. Here’s a detailed breakdown of the average costs for individual components of a kitchen remodel:

Cabinets

Cabinets are a significant investment in any kitchen remodel, typically accounting for 25% to 40% of the total project cost. The cost of cabinets varies widely depending on the material, style, size, and complexity of the design.

Average Range: $2,500 – $10,000

Factors Affecting Cost

Material: High-end materials like solid wood or custom-made cabinets will cost more than basic laminate or stock cabinets.

Style: Shaker-style cabinets are popular and relatively affordable, while ornate or highly customized designs can be significantly more expensive.

Size: A larger kitchen will require more cabinets, increasing the overall cost.

Countertops

Countertops are another major expense in a kitchen remodel, typically accounting for 15% to 25% of the total project cost. The choice of countertop material significantly impacts the overall price.

Average Range: $1,500 – $5,000

Factors Affecting Cost

Material: Granite and quartz countertops are popular and expensive, while laminate or butcher block countertops are more affordable options.

Edge Treatment: The type of edge treatment, such as a beveled or ogee edge, can add to the cost.

Size: A larger kitchen will require a larger countertop, increasing the overall cost.

Appliances

Appliances are a crucial aspect of any kitchen, and their cost can vary depending on the brand, features, and size.

Average Range: $1,000 – $5,000

Factors Affecting Cost

Brand: Premium brands like Viking or Wolf will cost more than mid-range or budget-friendly appliances.

Features: Appliances with advanced features, such as self-cleaning ovens or induction cooktops, will be more expensive than basic models.

Size: Larger appliances, such as a double oven or professional-grade refrigerator, will cost more than standard-sized models.

Flooring

Flooring plays a significant role in the overall aesthetics and durability of a kitchen. The cost of flooring varies depending on the material, style, and installation complexity.

Average Range: $500 – $2,000

Factors Affecting Cost

Material: Tile, hardwood, and vinyl are popular flooring options, with varying price points. Hardwood is generally the most expensive, while vinyl is the most affordable.

Style: Intricate patterns or custom-made designs can increase the cost.

Installation: Labor costs for professional installation can vary depending on the complexity of the flooring material and layout.

Lighting:

Lighting is essential for both functionality and ambiance in a kitchen. The cost of lighting depends on the type of fixtures, style, and quantity.

Average Range: $200 – $500

Factors Affecting Cost

Type of Fixtures: Recessed lighting, pendant lights, and under-cabinet lighting are common options, with varying price points.

Style: Designer or high-end lighting fixtures will cost more than basic models.

Quantity: The number of fixtures needed to adequately illuminate the kitchen will impact the overall cost.

Sink and Faucet

A new sink and faucet can significantly enhance the functionality and aesthetics of a kitchen. The cost varies depending on the material, style, and features.

Average Range: $200 – $500

Factors Affecting Cost

Material: Stainless steel is a popular and affordable option, while copper or cast iron sinks are more expensive.

Style: Farmhouse sinks or faucets with unique designs can increase the cost.

Features: Touchless faucets or sinks with integrated filtration systems can be more expensive.

Backsplash

A backsplash protects walls from splashes and enhances the overall kitchen design. The cost of a backsplash depends on the material, style, and installation complexity.

Average Range: $200 – $1,000

Factors Affecting Cost

Material: Tile, acrylic, or glass are common backsplash materials, with varying price points.

Style: Intricate patterns or custom-made backsplashes can increase the cost.

Installation: Labor costs for professional installation can vary depending on the complexity

DIY vs. Professional Services

Pros and Cons of a Do-It-Yourself Approach

While a DIY approach can save on labor costs, it comes with its challenges. Understanding the scope of the project and personal skill level is crucial to avoid costly mistakes that may outweigh potential savings.

Hiring Professionals for Quality and Time Efficiency

Professional contractors bring expertise to the table, ensuring a polished result and timely project completion. While their services may come at a premium, the quality and efficiency they offer can be well worth the investment.

Return on Investment (ROI)

Analyzing the Potential Increase in Property Value

A well-executed kitchen remodel has the potential to increase a rental property’s value. Understanding the market dynamics and potential return on investment is essential for making informed decisions.

Balancing Costs and Long-Term Benefits

Striking a balance between upfront costs and long-term benefits is critical. Investing in quality materials and professional services may incur higher initial expenses but can lead to lower maintenance costs and increased property value over time.

Common Mistakes to Avoid

Underestimating Hidden Costs

Unforeseen costs can quickly derail a remodeling budget. Anticipating potential challenges and budgeting for contingencies can prevent financial surprises.

Neglecting to Research and Compare Prices

Thorough research is the foundation of a well-informed remodel. Comparing prices for materials and services ensures that landlords secure the best value for their investment.

Failing to Plan for Contingencies

Murphy’s Law often applies to remodeling projects. Having a contingency plan in place for unexpected delays or issues can prevent stress and financial strain.

Real-life Case Studies

Showcasing Successful Kitchen Remodels on Rental Properties

Real-life examples provide valuable insights into successful kitchen remodels. Case studies will highlight cost-effective strategies implemented by landlords, offering practical inspiration for readers.

From creative material choices to strategic project management, showcasing cost-effective strategies emphasizes that a stylish and functional kitchen remodel can be achieved on a budget.

Financing Options

Exploring Loan Possibilities for Property Improvements

Financing a kitchen remodel can be achieved through various loan options. Exploring the best financing fit for the property and the landlord’s financial situation is a crucial step in the planning process.

Evaluating the Impact on Overall Investment Returns

Understanding the impact of financing on overall investment returns is essential. Striking a balance between obtaining necessary funds and avoiding excessive debt is key to a successful remodel.

Tips for Negotiating with Contractors

Securing Competitive Quotes

Obtaining quotes from multiple contractors enables landlords to compare prices and negotiate effectively. Transparency in communication and a clear understanding of project expectations contribute to successful negotiations.

Ensuring Transparency in Project Timelines and Costs

Clear communication about project timelines and costs is vital. Establishing expectations from the outset helps prevent misunderstandings and ensures a smoother remodeling process.

Future-Proofing Your Investment

Anticipating Evolving Design Trends

Kitchen design trends evolve, and future-proofing a remodel involves selecting elements with lasting appeal. Striking a balance between contemporary styles and timeless features ensures long-term tenant satisfaction.

Choosing Timeless Elements for Lasting Appeal

While incorporating modern elements is appealing, choosing timeless design features prevents the need for frequent updates. This approach contributes to the longevity of the remodel’s aesthetic appeal.

Sustainability in Kitchen Remodeling

Incorporating Eco-Friendly Materials and Appliances

Sustainability is increasingly valued by tenants. Exploring eco-friendly materials and energy-efficient appliances not only aligns with environmental considerations but can also attract environmentally conscious tenants.

Attracting Environmentally Conscious Tenants

Highlighting a commitment to sustainability can be a unique selling point. Attracting tenants who prioritize eco-friendly living can contribute to the property’s appeal and rental value.

Maintaining Compliance with Local Regulations

Understanding Building Codes and Permits

Navigating local building codes and obtaining necessary permits is a non-negotiable step in any remodel. Failing to comply with regulations can lead to costly legal issues and delays.

Navigating Potential Challenges in Compliance

Challenges in compliance may arise. Understanding potential hurdles and seeking guidance from local authorities ensures a smooth remodeling process.

Post-Remodel Evaluation

Assessing the Impact on Property Value and Tenant Satisfaction

After the dust settles, evaluating the impact of the remodel is crucial. Assessing both the increase in property value and tenant satisfaction provides valuable feedback for future enhancements.

Making Adjustments for Future Property Enhancements

Identifying areas for improvement post-remodel allows landlords to make necessary adjustments for future enhancements. This iterative approach contributes to ongoing property value growth.

Conclusion

In conclusion, a well-executed kitchen remodel in a rental property is a strategic investment that can enhance property value, attract quality tenants, and contribute to long-term financial success. By carefully considering factors such as location, budgeting strategies, and essential components, landlords can navigate the remodeling process with confidence.

FAQs

Q: How long does a typical kitchen remodel take in a rental property? A: The timeline for a kitchen remodel can vary based on factors such as project scope, contractor availability, and unforeseen challenges. On average, it may take several weeks to a few months.

Q: Is it worth investing in high-end appliances for a rental property kitchen? A: While high-end appliances can attract tenants, it’s essential to consider the target rental market. Striking a balance between quality and cost-effectiveness is key.

Q: Are there tax benefits for landlords who invest in property improvements? A: Depending on your location and tax regulations, there may be tax benefits for certain property improvements. Consult with a tax professional for personalized advice.

Q: How can I ensure a sustainable kitchen remodel without compromising style? A: Explore eco-friendly materials, energy-efficient appliances, and sustainable design practices. Many stylish options are available that align with sustainability goals.

Q: What is the most common mistake landlords make when remodeling a rental property kitchen? A: Underestimating hidden costs and failing to plan for contingencies are common mistakes. Thorough research and careful budgeting can help avoid these pitfalls.

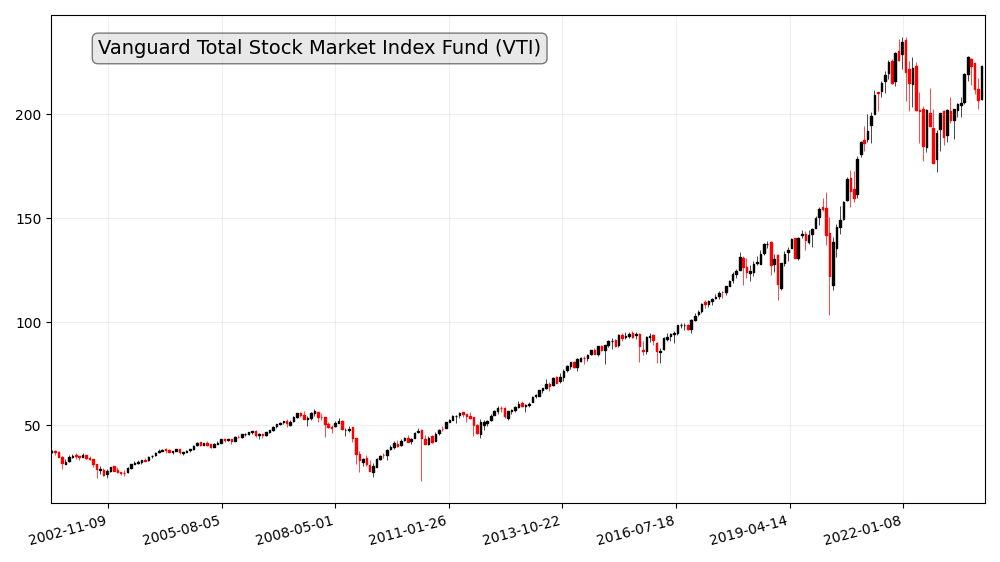

Investors worldwide are constantly seeking opportunities to grow their wealth, and understanding the dynamics of global stock market indices plays a crucial role in this pursuit. In this comprehensive exploration, we’ll delve into the basics of stock market indices, dissect major global indices, analyze factors influencing their movements, and discuss the future trends that could shape the financial landscape.

Exploring Global Stock Market Indices

Introduction

The world of finance is vast and dynamic, with global stock market indices acting as barometers for economic health and investor sentiment. This article aims to unravel the complexities surrounding these indices, providing both novice and seasoned investors with valuable insights.

Understanding Stock Market Indices

The Basics of Stock Market Indices

Before diving into the intricacies of global indices, let’s establish a foundational understanding of what stock market indices are and how they function.

How Indices Reflect Market Performance

Indices serve as benchmarks, reflecting the overall performance of a specific group of stocks. But how exactly do they capture the essence of market movements?

Significance of Global Stock Market Indices

Global stock market indices play a pivotal role in the financial world, offering several benefits:

Performance Indicators: They act as gauges of the overall health of the global economy, reflecting the collective performance of a wide range of companies across diverse industries and geographies.

Investment Benchmarks: They provide a yardstick against which investors can measure the performance of their own investment portfolios.

Risk Management Tools: They can be employed as risk management tools, allowing investors to diversify their portfolios across global markets and mitigate country-specific risks.

Major Global Stock Market Indices

As we embark on our journey, we’ll spotlight some of the most influential global indices, starting with the renowned S&P 500, offering a snapshot of the U.S. market.

S&P 500: A Snapshot of the U.S. Market

The S&P 500, comprising 500 of the largest publicly traded companies in the U.S., holds a special place in the hearts of investors.

The Standard & Poor’s 500, often abbreviated as the S&P 500, stands as a stalwart benchmark for assessing the health and performance of the U.S. stock market. Comprising 500 of the largest publicly traded companies in the United States, the S&P 500 provides investors, analysts, and policymakers with a comprehensive snapshot of the nation’s economic landscape. In this article, we will explore the significance, composition, and influence of the S&P 500 on the U.S. financial market.

Overview of the S&P 500:The S&P 500, launched in 1957, is a market-capitalization-weighted index that reflects the performance of a broad cross-section of industries. Its components include some of the most prominent and influential companies across various sectors, making it a reliable gauge of the overall health of the U.S. equity market.

Composition and Diversity:The diversity of the S&P 500 is one of its defining features. The index encompasses companies from sectors such as technology, healthcare, finance, consumer discretionary, and more. This broad representation helps mitigate the impact of poor performance in a single sector on the overall index.

Market Capitalization Weighting:The S&P 500 is a market-capitalization-weighted index, meaning that the companies with the highest market capitalization—calculated by multiplying the share price by the number of outstanding shares—have a more substantial impact on the index’s value. This approach reflects the market’s consensus on the relative importance of each included company.

Influence on Investment Strategies:Due to its diverse composition and broad representation of the U.S. economy, the S&P 500 plays a pivotal role in shaping investment strategies. Many index funds and exchange-traded funds (ETFs) are designed to replicate the performance of the S&P 500, providing investors with a convenient way to gain exposure to the overall U.S. equity market.

Economic Indicator:The S&P 500 is often regarded as a leading economic indicator. Changes in the index’s value are closely monitored by investors, economists, and policymakers to assess the overall economic health of the United States. A rising S&P 500 is generally considered a positive signal for the economy, while a declining index may indicate potential challenges.

Global Impact:Given the global nature of many S&P 500 companies, the index’s movements can have repercussions beyond U.S. borders. Investors worldwide pay attention to the S&P 500 as a barometer of global economic conditions, making it a crucial reference point in international financial markets.

Quarterly Earnings Reports:The S&P 500 companies, being some of the largest and most influential in the world, release quarterly earnings reports. These reports can significantly impact the index’s value, as investors assess the financial health and performance of these key players.

Volatility and Risk Management:Investors often turn to the S&P 500 for insights into market volatility and risk management. The CBOE Volatility Index (VIX), often referred to as the “fear index,” is derived from S&P 500 options prices and serves as a gauge of market expectations for future volatility.

FTSE 100: Unveiling the British Market

Across the Atlantic, the FTSE 100 takes center stage. What insights does this index provide into the British market, and why is it closely monitored by investors worldwide?

The Financial Times Stock Exchange 100 Index, commonly known as the FTSE 100, stands as a prominent indicator of the health and performance of the British stock market. Comprising 100 of the largest publicly traded companies on the London Stock Exchange, the FTSE 100 is a vital benchmark for investors, analysts, and policymakers seeking insights into the economic landscape of the United Kingdom. In this article, we will explore the significance, composition, and impact of the FTSE 100 on the British financial market.

Historical Background: Established in 1984, the FTSE 100 has become synonymous with the British stock market. The index is maintained by the FTSE Russell, a global index provider, and is widely recognized both domestically and internationally.

Composition and Diversity: The FTSE 100 is composed of the 100 largest companies listed on the London Stock Exchange, measured by market capitalization. These companies span various sectors, including finance, energy, healthcare, consumer goods, and telecommunications. The diverse representation provides a comprehensive view of the UK’s economic landscape.

Market Capitalization Weighting: Similar to the S&P 500 in the United States, the FTSE 100 is a market-capitalization-weighted index. This means that companies with higher market capitalization exert a more significant influence on the index’s value. As such, changes in the share prices of large companies can have a substantial impact on the overall index.

Global Recognition: The FTSE 100 is recognized globally as a key indicator of the British market’s performance. Its movements are closely watched by investors worldwide, providing insights into the health of the UK economy and serving as a crucial reference point for international investment decisions.

Economic Barometer: The FTSE 100 serves as a barometer for the broader UK economy. Movements in the index are often interpreted as indicators of economic strength or challenges. A rising FTSE 100 is generally seen as a positive signal, reflecting optimism about economic prospects, while a declining index may suggest concerns or uncertainties.

Influence on Investment Strategies: The FTSE 100 is a critical factor in shaping investment strategies for both individual and institutional investors. Funds, such as index trackers and ETFs, are designed to replicate the performance of the FTSE 100, allowing investors to gain exposure to a broad cross-section of the British market.

Currency and Global Markets: As the FTSE 100 is composed of multinational companies, its performance is influenced not only by domestic factors but also by global economic conditions. Changes in currency values, global trade dynamics, and geopolitical events can impact the FTSE 100, making it sensitive to a range of international factors.

Volatility and Risk Management: Investors often turn to the FTSE 100 as a measure of market volatility and for risk management purposes. The volatility index, derived from FTSE 100 options prices, provides insights into market expectations for future price fluctuations.

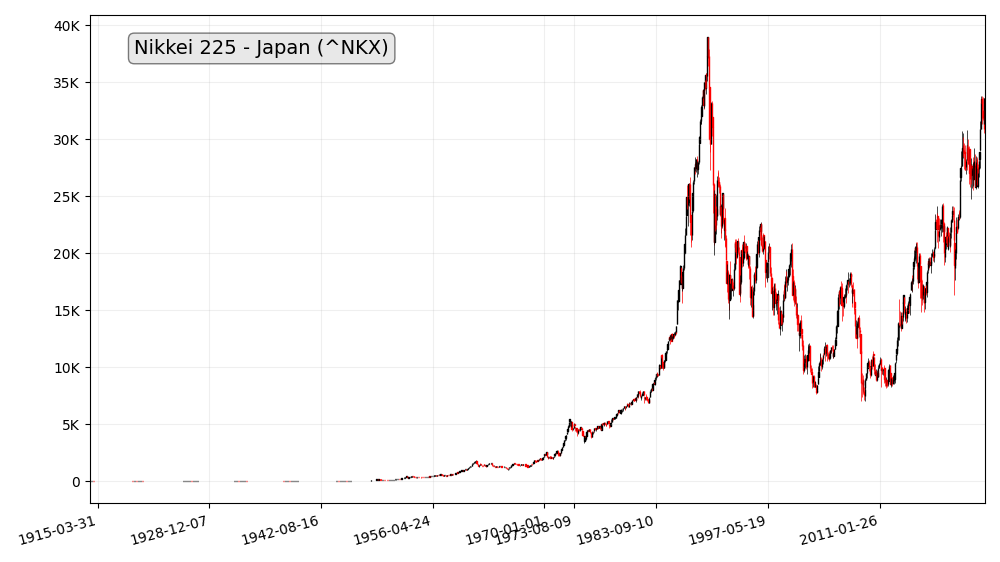

Nikkei 225: Insights into Japanese Equities

Our exploration extends to the East with a focus on the Nikkei 225, providing a window into the Japanese stock market and its unique characteristics.

The Nikkei 225, Japan’s premier stock market index, is a beacon that illuminates the performance and trends of the country’s equity market. Comprising 225 of the largest and most influential companies listed on the Tokyo Stock Exchange, the Nikkei 225 serves as a key indicator for investors, analysts, and policymakers seeking a nuanced understanding of Japan’s economic landscape. In this article, we will delve into the significance, composition, and impact of the Nikkei 225 on Japanese equities.

Historical Evolution: The Nikkei 225, short for the Nikkei Stock Average, made its debut in 1950 and has since become synonymous with Japan’s financial markets. It is managed and calculated by the Nikkei Inc., a media company that also oversees other financial indices and information services.

Composition and Selection Criteria: The Nikkei 225 includes 225 of the largest and most liquid companies listed on the Tokyo Stock Exchange. These companies span diverse sectors, including automotive, technology, finance, and manufacturing. The selection is based on market capitalization, ensuring that the index provides a comprehensive representation of the Japanese stock market.

Market Capitalization Weighting: Similar to other major indices like the S&P 500, the Nikkei 225 is a price-weighted index. This means that the impact of each component on the index is proportional to its stock price. While differing from the market-capitalization-weighted approach, it still offers a valuable snapshot of the overall market trends.

Economic Indicator: The Nikkei 225 is not only a reflection of the Japanese stock market but is often viewed as an economic indicator for the nation. Movements in the index are closely observed for insights into Japan’s economic health, providing an indication of investor sentiment, economic growth, and corporate performance.

Influence on Investment Strategies: Investors, both domestic and international, frequently use the Nikkei 225 as a benchmark for their investment strategies. Financial products such as index funds and exchange-traded funds (ETFs) are designed to replicate the performance of the Nikkei 225, allowing investors to gain exposure to a broad array of Japanese equities.

Global Recognition: The Nikkei 225 enjoys global recognition as a key indicator of the Japanese market. Its movements are closely monitored by international investors and fund managers, making it an essential reference point for those looking to understand and navigate the Japanese economic landscape.

Sensitivity to Economic Factors: Given Japan’s position as one of the world’s largest economies, the Nikkei 225 is sensitive to a variety of economic factors. Changes in interest rates, currency values, and global economic conditions can all impact the index, making it a dynamic and responsive indicator.

Volatility and Risk Management: Like other major indices, the Nikkei 225 serves as a tool for assessing market volatility and managing investment risk. The volatility index derived from Nikkei 225 options prices, known as the “Nikkei Volatility,” provides insights into market expectations for future price fluctuations.

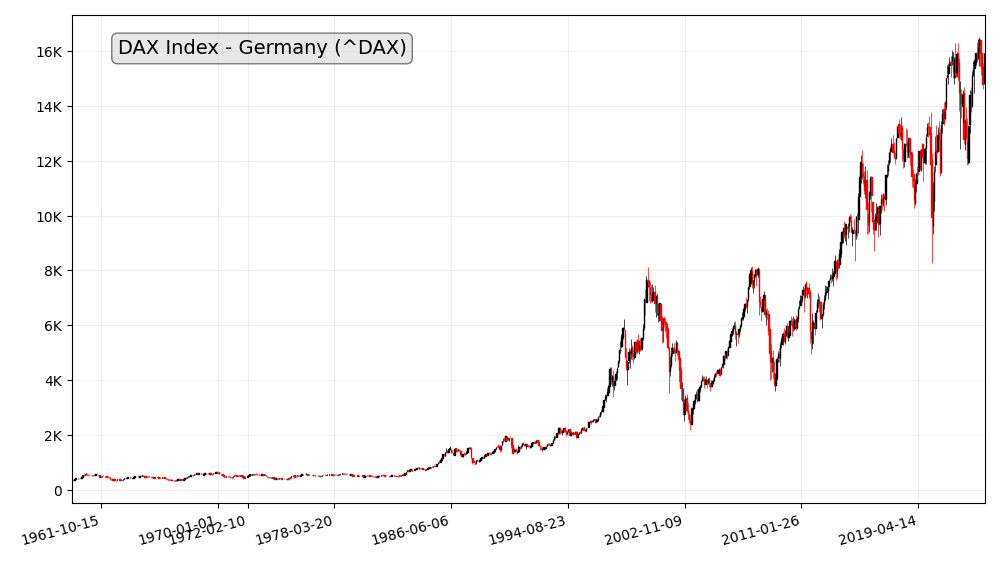

DAX Index: A Glimpse into German Stocks

Heading to Europe, the DAX Index reveals the performance of German stocks. What economic factors influence its movements, and why is it vital for global investors?

The DAX Index, standing as the benchmark for the German stock market, provides investors, analysts, and policymakers with a comprehensive view of the performance and trends within Germany’s equity landscape. Comprising 30 of the largest and most liquid companies listed on the Frankfurt Stock Exchange, the DAX Index is a crucial indicator for those seeking insights into Germany’s economic health. In this article, we will explore the significance, composition, and impact of the DAX Index on German stocks.

Historical Origins: The DAX, short for Deutscher Aktienindex (German Stock Index), was introduced in 1988. Developed and maintained by the Frankfurt Stock Exchange, the DAX quickly became the primary benchmark for tracking the performance of Germany’s leading publicly traded companies.

Composition and Selection Criteria: The DAX Index comprises 30 blue-chip companies listed on the Frankfurt Stock Exchange. These companies, referred to as the DAX 30, represent a diverse range of sectors, including automotive, finance, technology, and healthcare. The selection criteria are based on factors such as market capitalization, liquidity, and historical trading volume.

Market Capitalization Weighting: Similar to other major indices, the DAX is a market-capitalization-weighted index. This means that the impact of each component on the index is proportionate to its market capitalization. As a result, larger companies hold more significant influence over the overall value of the index.

Economic Indicator: The DAX Index is not merely a reflection of the German stock market; it serves as a crucial economic indicator for the nation. Movements in the index are often interpreted as signals of Germany’s economic health, providing insights into investor sentiment, economic growth, and corporate performance.

Influence on Investment Strategies: The DAX 30 plays a pivotal role in shaping investment strategies for both domestic and international investors. Financial instruments such as exchange-traded funds (ETFs) and index funds are designed to replicate the performance of the DAX, allowing investors to gain exposure to a diversified portfolio of German equities.

Global Recognition: The DAX enjoys global recognition as a leading indicator of the German stock market. Its movements are closely monitored by international investors and fund managers, offering insights into the economic strength and performance of one of Europe’s largest economies.

Sensitivity to Economic Factors: Given Germany’s position as an economic powerhouse in Europe, the DAX is sensitive to various economic factors. Changes in interest rates, currency values, and global economic conditions can influence the performance of the DAX, making it a dynamic and responsive indicator.

Volatility and Risk Management: As with other major indices, the DAX serves as a tool for assessing market volatility and managing investment risk. The Volatility Index (VDAX), derived from DAX options prices, offers insights into market expectations for future price fluctuations, aiding investors in risk assessment and management.

NASDAQ Composite Index

The Nasdaq Composite Index tracks the performance of all stocks listed on the Nasdaq stock exchange, including large, mid-cap, and small-cap companies. It is heavily weighted towards technology stocks.

The NASDAQ Composite Index, often referred to simply as the NASDAQ, stands as a beacon of technological and innovative prowess within the financial markets. Comprising thousands of companies, it is a barometer for the performance of the technology sector and a reflection of the entrepreneurial spirit that defines the modern economy. In this article, we will explore the significance, composition, and impact of the NASDAQ Composite Index on the world of finance.

Historical Roots: The NASDAQ Composite Index, launched in 1971, is one of the younger major stock indices. Operated by the NASDAQ OMX Group, it was the first electronic stock market, pioneering a new era in trading by introducing electronic communication networks (ECNs) and revolutionizing how stocks are bought and sold.

Composition and Diversity: The NASDAQ Composite is not limited to a specific number of companies; instead, it includes all stocks listed on the NASDAQ stock exchange. This diversity allows the index to represent a wide range of sectors, with a particular emphasis on technology, biotechnology, and internet-based companies.

Technology and Innovation Hub: Often dubbed as the “tech-heavy” index, the NASDAQ Composite is synonymous with innovation. It includes some of the world’s most renowned technology giants, such as Apple, Amazon, Microsoft, and Alphabet (Google), as well as a plethora of smaller, cutting-edge companies driving advancements in various industries.

Market Capitalization Weighting: The NASDAQ Composite is a market-capitalization-weighted index, meaning that companies with higher market capitalizations carry more significant influence over the index’s value. This structure reflects the market’s collective opinion on the relative importance of each included company.

Influence on Investment Strategies: The NASDAQ Composite plays a crucial role in shaping investment strategies, particularly for those seeking exposure to the dynamic world of technology and innovation. Numerous exchange-traded funds (ETFs) and mutual funds are designed to replicate the performance of the NASDAQ, providing investors with diversified access to this influential sector.

Entrepreneurial Spirit: Beyond being a mere financial indicator, the NASDAQ Composite embodies the entrepreneurial spirit. It is a platform where start-ups and emerging companies can go public and raise capital, contributing to the continuous evolution and transformation of the global business landscape.

Global Recognition: The NASDAQ Composite is recognized globally as a key benchmark for technology and innovation. Its movements are closely monitored by investors, analysts, and policymakers worldwide, offering insights into the health and trends of the tech sector and the broader economy.

Volatility and Risk Perception: The NASDAQ Composite’s association with technology and growth-oriented companies makes it inherently more volatile than some other indices. The Volatility Index (VXN), derived from NASDAQ options prices, helps investors gauge market expectations for future price fluctuations and manage the associated risks.

Biotechnology and Healthcare: In addition to technology, the NASDAQ Composite has a significant representation of biotechnology and healthcare companies. This inclusion further amplifies its role as a comprehensive indicator of innovation across various sectors.

Dow Jones Industrial Average

The Dow Jones Industrial Average (DJIA) is a price-weighted index of 30 large-cap companies listed on stock exchanges in the United States. It is one of the oldest and most widely followed stock market indices.

The Dow Jones Industrial Average (DJIA), often referred to simply as the Dow, is a venerable and iconic index that has been a stalwart presence in the world of finance for over a century. Comprising 30 of the largest and most influential publicly traded companies in the United States, the Dow is a barometer that provides investors, analysts, and the general public with insights into the overall health of the U.S. stock market. In this article, we will explore the historical significance, composition, and impact of the Dow Jones Industrial Average.

Historical Origins: Created in 1896 by financial journalist Charles Dow and his business partner Edward Jones, the Dow Jones Industrial Average is one of the oldest and most widely followed stock market indices. Initially comprising just 12 companies, the Dow has evolved over the years to include 30 blue-chip companies representing various sectors of the U.S. economy.

Composition and Selection Criteria: The Dow’s composition includes companies that are leaders in their respective industries, reflecting the overall health of the U.S. economy. While not exhaustive, the Dow’s 30 companies are chosen based on their reputation, size, and prominence. Changes to the Dow’s composition are infrequent and are made by the Dow Jones Index Committee.

Market Price-Weighted Index: The Dow is a price-weighted index, meaning that the relative influence of each component is determined by its stock price rather than its market capitalization. This makes it unique among major indices, such as the S&P 500, which are market-capitalization-weighted. The Dow’s structure can lead to a higher influence from higher-priced stocks.

Diverse Sector Representation: The Dow is designed to represent a cross-section of the U.S. economy, and as such, it includes companies from various sectors, including technology, healthcare, finance, and manufacturing. This diversity allows the index to provide a snapshot of the overall economic health of the nation.

Economic Indicator: Widely regarded as a key economic indicator, the Dow is often used to gauge the general health of the U.S. stock market and, by extension, the broader economy. Movements in the Dow are closely monitored for insights into investor sentiment, economic trends, and potential market shifts.

Influence on Investment Strategies: The Dow plays a significant role in shaping investment strategies for both individual and institutional investors. Investment products such as index funds and exchange-traded funds (ETFs) are designed to replicate the performance of the Dow, allowing investors to gain exposure to a diverse array of U.S. blue-chip stocks.

Global Recognition: The Dow Jones Industrial Average is recognized globally as a symbol of U.S. economic strength. Its movements are closely watched by investors worldwide, and its influence extends beyond American borders, impacting international markets and investment decisions.

Volatility and Risk Perception: The Dow’s status as a leading indicator makes it a useful tool for assessing market volatility and managing investment risk. The CBOE Volatility Index (VIX), often referred to as the “fear index,” is derived from options prices on the S&P 500 but is widely used as a gauge of overall market volatility, including the Dow.

Hang Seng Index

The Hang Seng Index is a key benchmark for the Hong Kong stock market, tracking the performance of 50 of the largest and most liquid companies listed on the Hong Kong Stock Exchange.

The Hang Seng Index (HSI), a cornerstone of the financial markets in Hong Kong, stands as a robust indicator of the region’s economic health and market performance. Comprising a diverse array of leading companies, the HSI provides investors, analysts, and policymakers with a comprehensive snapshot of Hong Kong’s dynamic and influential financial landscape. In this article, we will explore the significance, composition, and impact of the Hang Seng Index.

Historical Evolution: Established in 1969 by the Hang Seng Bank, the Hang Seng Index has grown to become a key benchmark for the Hong Kong Stock Exchange (HKEX). Initially starting with only 33 constituents, the index has expanded over the years to include a broader spectrum of companies representing various industries.

Composition and Selection Criteria: The Hang Seng Index comprises 50 of the largest and most liquid companies listed on the HKEX. These companies are selected based on factors such as market capitalization, trading volume, and overall market influence. The diverse composition of the HSI includes companies from sectors such as finance, real estate, technology, and utilities.

Market Capitalization Weighting: Similar to other major indices globally, the Hang Seng Index is a market-capitalization-weighted index. This means that the influence of each component on the index is proportional to its market capitalization. Larger companies, by market value, have a more significant impact on the index’s movements.

Influence on Hong Kong’s Financial Landscape: The Hang Seng Index plays a pivotal role in shaping Hong Kong’s financial landscape. As a reflection of the region’s economic health, the HSI is a barometer for investor sentiment and a crucial indicator for policymakers assessing the overall stability and performance of the Hong Kong economy.

Global Recognition: While primarily focused on Hong Kong-listed companies, the Hang Seng Index enjoys global recognition. Its movements are closely monitored by international investors, fund managers, and analysts, serving as a vital reference point for those seeking insights into the economic health and market trends of the Asia-Pacific region.

China’s Impact on the HSI: Given Hong Kong’s proximity to mainland China, the Hang Seng Index is influenced by developments in the broader Chinese economy. Changes in economic policies, trade relations, and geopolitical events impacting China can have a ripple effect on the HSI, making it sensitive to regional and global economic dynamics.

Volatility and Risk Perception: As with any major index, the Hang Seng Index is subject to market volatility. The Volatility Index (VHSI), derived from options prices on the HSI, provides insights into market expectations for future price fluctuations, aiding investors in assessing and managing risk.

Technology and Financial Sector Emphasis: In recent years, the Hang Seng Index has seen an increased emphasis on technology and financial sector companies, reflecting the evolving nature of the Hong Kong economy. The inclusion of innovative and dynamic companies in these sectors aligns with global trends in technology-driven economies.

Shanghai Stock Exchange Composite Index (SSE 300)

The SSE 300 is a stock market index that tracks the performance of 300 of the largest and most liquid A-shares listed on the Shanghai Stock Exchange (SSE). It is a key benchmark for the Chinese equity market.

The Hang Seng Index (HSI), a cornerstone of the financial markets in Hong Kong, stands as a robust indicator of the region’s economic health and market performance. Comprising a diverse array of leading companies, the HSI provides investors, analysts, and policymakers with a comprehensive snapshot of Hong Kong’s dynamic and influential financial landscape. In this article, we will explore the significance, composition, and impact of the Hang Seng Index.

Historical Evolution: Established in 1969 by the Hang Seng Bank, the Hang Seng Index has grown to become a key benchmark for the Hong Kong Stock Exchange (HKEX). Initially starting with only 33 constituents, the index has expanded over the years to include a broader spectrum of companies representing various industries.

Composition and Selection Criteria: The Hang Seng Index comprises 50 of the largest and most liquid companies listed on the HKEX. These companies are selected based on factors such as market capitalization, trading volume, and overall market influence. The diverse composition of the HSI includes companies from sectors such as finance, real estate, technology, and utilities.

Market Capitalization Weighting: Similar to other major indices globally, the Hang Seng Index is a market-capitalization-weighted index. This means that the influence of each component on the index is proportional to its market capitalization. Larger companies, by market value, have a more significant impact on the index’s movements.

Influence on Hong Kong’s Financial Landscape: The Hang Seng Index plays a pivotal role in shaping Hong Kong’s financial landscape. As a reflection of the region’s economic health, the HSI is a barometer for investor sentiment and a crucial indicator for policymakers assessing the overall stability and performance of the Hong Kong economy.

Global Recognition: While primarily focused on Hong Kong-listed companies, the Hang Seng Index enjoys global recognition. Its movements are closely monitored by international investors, fund managers, and analysts, serving as a vital reference point for those seeking insights into the economic health and market trends of the Asia-Pacific region.

China’s Impact on the HSI: Given Hong Kong’s proximity to mainland China, the Hang Seng Index is influenced by developments in the broader Chinese economy. Changes in economic policies, trade relations, and geopolitical events impacting China can have a ripple effect on the HSI, making it sensitive to regional and global economic dynamics.

Volatility and Risk Perception: As with any major index, the Hang Seng Index is subject to market volatility. The Volatility Index (VHSI), derived from options prices on the HSI, provides insights into market expectations for future price fluctuations, aiding investors in assessing and managing risk.

Technology and Financial Sector Emphasis: In recent years, the Hang Seng Index has seen an increased emphasis on technology and financial sector companies, reflecting the evolving nature of the Hong Kong economy. The inclusion of innovative and dynamic companies in these sectors aligns with global trends in technology-driven economies.

MSCI World Index

The MSCI World Index is a broad-based index that tracks the performance of large and mid-cap stocks from 23 developed countries. It is widely considered the most representative benchmark for the global equity market.

The MSCI World Index stands as a powerful and influential benchmark in the realm of global investing, providing investors with a panoramic view of equities from around the world. Comprising a diverse array of companies representing both developed and emerging markets, the MSCI World Index serves as a comprehensive indicator for investors, analysts, and policymakers seeking insights into the performance and trends of the global equity landscape. In this article, we will explore the historical significance, composition, and impact of the MSCI World Index.

Historical Evolution: The MSCI World Index, launched in 1969 by Morgan Stanley Capital International (MSCI), has evolved over the decades to become a prominent benchmark for global equities. Initially encompassing only five developed markets, the index has expanded its scope to include companies from 23 developed countries, providing a more comprehensive representation of the global equity market.

Composition and Selection Criteria: The MSCI World Index comprises a broad spectrum of companies from developed countries, including the United States, Japan, the United Kingdom, Germany, and others. The index covers various sectors such as technology, finance, healthcare, and consumer goods. Companies are selected based on their market capitalization, liquidity, and overall market influence.

Market Capitalization Weighting: The MSCI World Index is a market-capitalization-weighted index, mirroring the methodology of many major indices globally. This means that the influence of each constituent on the index is proportional to its market capitalization. Larger companies, by market value, exert a more significant impact on the overall value of the MSCI World Index.

Global Representation: One of the defining features of the MSCI World Index is its global representation. The index includes companies from North America, Europe, Asia, and the Pacific region, providing investors with exposure to a diverse range of economies, industries, and currencies. This global scope makes the MSCI World Index a comprehensive tool for assessing worldwide market trends.

Influence on Investment Strategies: The MSCI World Index is integral to shaping investment strategies for institutional and individual investors alike. Numerous investment products, including index funds and exchange-traded funds (ETFs), are designed to replicate the performance of the MSCI World Index, offering investors a convenient way to gain diversified exposure to global equities.

Economic Indicator: Widely recognized as a key economic indicator, the MSCI World Index is often used to assess the overall health of the global economy. Movements in the index are closely monitored for insights into investor sentiment, economic growth prospects, and potential market shifts.

Diversity and Sector Allocation: The MSCI World Index’s composition spans a multitude of industries, reflecting the diversity of the global economy. Investors can find companies from technology, healthcare, financial services, consumer discretionary, and other sectors, offering a well-rounded representation of the world’s major industries.

Volatility and Risk Management: As a reflection of global equities, the MSCI World Index can be subject to market volatility. Investors often refer to volatility indices derived from options on the MSCI World Index, such as the MSCI World Volatility Index, to gauge market expectations for future price fluctuations and manage associated risks.

Investing in Global Stock Market Indices

Direct Investment through Index Funds or ETFs

Investors can directly invest in global stock market indices through index funds or exchange-traded funds (ETFs). These investment vehicles passively track a particular index, providing a convenient and cost-effective way to gain exposure to a diversified basket of global stocks.

Indirect Investment through Managed Funds or Strategies

Alternatively, investors can opt for managed funds or strategies that actively seek to outperform global stock market indices. These strategies may employ various investment techniques, such as stock picking, sector rotation, or tactical asset allocation, to generate excess returns.

Potential Risks and Considerations of Global Stock Market Investing

Investing in global stock markets involves inherent risks, including:

Currency Fluctuations and Exchange Rate Risks

Investments in foreign markets are exposed to currency fluctuations, which can erode returns or amplify losses due to exchange rate movements.

Political and Economic Risks of Foreign Markets

Political instability, economic downturns, or regulatory changes in foreign countries can adversely impact the performance of overseas investments.

Conclusion

In conclusion, global stock market indices serve as invaluable tools for investors navigating the complex financial landscape. Understanding the nuances of these indices empowers individuals to make informed investment decisions, seizing opportunities while mitigating risks.

FAQs

What is the significance of tracking global stock market indices?

Understanding the broader market trends helps investors make informed decisions and identify potential investment opportunities.

How often do stock market indices experience significant changes?

The frequency of changes varies, influenced by economic events, geopolitical factors, and market sentiment.

Are there any risks associated with investing in global indices?

Yes, like any investment, global indices carry risks, including market volatility and geopolitical uncertainties.

What role do technological advancements play in shaping index movements?

Technological advancements, such as algorithmic trading and artificial intelligence, can impact market dynamics and index movements.

How can investors navigate market volatility when investing in global indices?

Diversification, strategic planning, and staying informed are key strategies to navigate market volatility.

Land banking, a strategic investment practice gaining popularity in real estate, involves acquiring undeveloped land for future use or resale. In this comprehensive guide, we’ll navigate through the intricate process of land banking, providing valuable insights and step-by-step instructions for individuals looking to venture into this promising investment strategy.

Step-by-Step Guide to Land Banking

Introduction

Land banking is a proactive investment approach where individuals purchase parcels of undeveloped land with the anticipation of future appreciation. It’s a long-term strategy that requires careful consideration and planning. For those unfamiliar with the concept, land banking can be a powerful tool in diversifying investment portfolios.

Benefits of Land Banking

Potential for Capital Appreciation

One of the primary attractions of land banking is the potential for significant capital appreciation over time. Unlike developed properties that may face depreciation, well-selected land in growing areas tends to increase in value as demand for space rises.

Land has historically exhibited a tendency to appreciate in value over time, driven by population growth, urbanization, and economic development. Investing in undeveloped land can potentially capitalize on this long-term appreciation trend.

Mitigating Risks in the Real Estate Market

Land banking serves as a buffer against the volatility of the real estate market. While property values may fluctuate, strategically chosen land has the potential to appreciate steadily, providing a stable long-term investment.

Land banking can provide diversification within a real estate investment portfolio, as its performance is not directly correlated with the fluctuations of other asset classes.

Inflation Hedge

Land is often considered a hedge against inflation, as its value tends to rise with the overall cost of living. Holding land as an investment can help protect purchasing power over time.

Passive Income Potential

Once the land is developed or sold, it can generate passive income for the investor in the form of rent, royalties, or lump sum proceed

Selecting the Right Location

Researching Growth Potential

Identifying regions with anticipated growth is crucial for successful land banking. Thorough research into economic indicators, population trends, and local development plans is essential.

Analyzing Local Market Trends

Understanding current and future market trends in the chosen location helps in making informed decisions. Analyzing factors such as demand, supply, and pricing dynamics is key to successful land banking.

Considering Infrastructure Development

Areas undergoing infrastructure development often present lucrative opportunities for land banking. Proximity to transportation hubs, educational institutions, and commercial centers can significantly impact the land’s future value.

Legal Considerations

Understanding Zoning Laws

Navigating zoning laws is fundamental to land banking. Investors must be aware of the permissible uses for the land and any potential changes in zoning regulations.

Checking Land Use Restrictions

In addition to zoning, land use restrictions can impact the development potential of the acquired land. A thorough understanding of these restrictions is crucial for effective land banking.

Securing Necessary Permits

Ensuring compliance with local regulations requires obtaining the necessary permits. This includes approvals for land development and adherence to environmental standards.

Exit Strategies for Land Banking

Land bankers have several exit strategies to realize the value of their investment:

Selling the Land to Developers or Investors

Once the land’s value has appreciated significantly, land bankers can sell it to developers or other investors who intend to develop it. This strategy can generate substantial profits if the land has experienced significant appreciation.

Subdividing and Selling Smaller Parcels

Land bankers can subdivide the land into smaller parcels and sell them to individual buyers or smaller developers. This strategy can provide more flexibility and potentially generate higher overall returns.

Leasing the Land for Temporary Use

Land bankers can lease the land for temporary use, such as agricultural purposes or non-permanent structures. This strategy can generate income while the land bankers wait for its value to appreciate.

Financial Planning for Land Banking

Setting a Budget

Establishing a realistic budget is the foundation of successful land banking. It involves considering the initial land acquisition costs, development expenses, and holding costs.

Evaluating Financing Options

Investors should explore various financing options to determine the most suitable for their land banking venture. This may include traditional loans, private financing, or partnerships.

Projecting Long-Term Costs

Anticipating long-term costs is essential for financial planning. This includes holding costs, property taxes, and any potential development expenses that may arise over time.

Steps in Acquiring Land

Identifying Suitable Parcels

Careful consideration of the type and location of the land is crucial. Investors should focus on parcels with growth potential and align with their overall investment goals.

Investors should conduct extensive research to understand the surrounding area, demographic trends, and infrastructure development plans. They should also consult with local real estate experts to gain insights into market conditions and zoning regulations.

Negotiating with Landowners

Successful land banking often involves skillful negotiation with landowners. Establishing favorable terms for the acquisition is a critical aspect of the process.

Approaching Landowners and Establishing Negotiation Strategy

Investors should approach landowners with a clear understanding of the land’s potential value and their development plans. They should also be prepared to negotiate flexibly to reach a mutually beneficial agreement.

Conducting Title Search and Property Inspection

Before closing the deal, it is essential to conduct a thorough title search to ensure there are no encumbrances or liens on the property. Additionally, a property inspection should be conducted to identify any potential environmental or structural issues.

Securing Financing and Closing the Deal

Land banking often requires substantial upfront capital, and investors may need to secure financing to complete the purchase. Once the financing is in place, the parties can move forward with closing the deal and transferring ownership of the land.

Conducting Due Diligence

Thorough due diligence is imperative before finalizing any land purchase. This includes surveys, environmental assessments, and title searches to uncover any potential issues.

Professional Assistance

Working with Real Estate Experts

Engaging the services of experienced real estate professionals can provide valuable insights. Real estate agents, appraisers, and consultants can contribute to informed decision-making.

Seeking Legal Advice

Given the legal complexities of land acquisition and development, seeking legal advice is essential. Legal experts can navigate through the intricacies of zoning laws and land use restrictions.

Collaborating with Financial Consultants

Financial consultants can assist in developing a sound financial strategy for land banking. They can provide insights into financing options and long-term financial planning.

Managing and Developing the Land

Creating a Development Plan

Having a clear development plan is essential for maximizing the land’s potential. This includes considerations for residential, commercial, or mixed-use development.

Implementing Sustainable Practices

Incorporating sustainable practices not only aligns with environmental consciousness but can also enhance the land’s overall value. Investors should explore eco-friendly development options.

Monitoring Market Trends for Optimal Timing

Staying attuned to market trends helps in determining the optimal timing for land development or resale. Flexibility in adapting to market dynamics is key to success.

Risks and Challenges

Market Fluctuations

Land values can be subject to market fluctuations. Understanding the factors influencing these fluctuations is crucial for risk management.

Environmental Concerns

Environmental issues, such as contamination or ecological restrictions, can impact land usability. Conducting thorough environmental assessments is vital.

Regulatory Changes

Changes in zoning laws or land use regulations can pose challenges to land banking. Staying informed about potential regulatory shifts is essential.

Myths and Misconceptions

Addressing Common Misconceptions About Land Banking

Dispelling myths and clarifying misconceptions is vital. Common misunderstandings about land banking can deter potential investors from exploring this lucrative strategy.

Land Banking Yields Quick Returns

One of the prevalent misconceptions is that land banking generates quick returns similar to flipping properties or short-term investments. In reality, land banking is a patient and long-term strategy. Investors must be prepared to hold the land for an extended period, sometimes years, waiting for the right conditions for development and appreciation.

Guaranteed Profit

While land banking has the potential for profit, there are no guarantees. The success of the investment depends on various factors such as location, market conditions, and the overall economic environment. Investors must conduct thorough research and due diligence to mitigate risks and make informed decisions.

Land Banking is Speculative and Risky

Some perceive land banking as a speculative and risky venture akin to gambling. While all investments carry inherent risks, land banking, when done strategically, aims to mitigate certain risks associated with immediate development. Patiently waiting for the right market conditions and development opportunities can contribute to a more stable investment.

No Involvement in the Local Community

Another misconception is that land banking involves passive investment without contributing to the local community. In reality, both private investors and local governments engaging in land banking can significantly impact communities. Well-planned land banking can lead to thoughtful urban development, green spaces, and infrastructure improvements.

Land Banking is Only for Large Investors

Some believe that land banking is exclusively for large-scale investors or corporations. While institutional investors may engage in land banking, it is not limited to them. Individual investors can also participate, provided they conduct thorough research, understand local regulations, and have a long-term investment horizon.

Land Banking Always Requires Huge Capital

Contrary to the belief that land banking demands massive capital, there are opportunities for investors with varying budgets. The key is to identify strategically located parcels within the investor’s financial reach. Additionally, some investors participate in land banking through collective investment vehicles, such as real estate investment trusts (REITs).

Land Banking Involves Neglecting the Land

Some assume that land banking means leaving the acquired land untouched and neglected. In reality, responsible land banking involves maintaining the land, adhering to any necessary maintenance or environmental regulations, and ensuring that the property is well-positioned for future development.

Land Banking Always Requires Development

Another misconception is that land banking mandates eventual development. In truth, the decision to develop the land rests with the investor or governing body. Holding land can provide flexibility, allowing stakeholders to respond to changing market conditions or community needs.

Providing Clarity on Potential Challenges

Transparent communication about potential challenges fosters realistic expectations. Investors should be aware of the complexities involved in land banking.

Future Trends in Land Banking

Technological Advancements in Land Management

Technological innovations in land management are shaping the future of land banking. Investors should stay abreast of these advancements for a competitive edge.

Evolving Market Dynamics

The real estate landscape is dynamic, with constant changes in market dynamics. Being aware of evolving trends is crucial for adapting land banking strategies.

Conclusion

In conclusion, land banking is a strategic and potentially lucrative investment option. By carefully selecting the right location, navigating legal considerations, and implementing a sound financial plan, investors can unlock the full potential of land banking. A comparative analysis with other investments further underscore the value of this approach.

FAQs

Is land banking suitable for all investors?

Land banking can be suitable for investors seeking long-term, stable returns. However, individual preferences and risk tolerance should be considered.

How long should one hold land before selling or developing it?

The ideal holding period varies based on market conditions and the investor’s goals. Patience is often a key factor in maximizing returns.

What are the tax advantages associated with land banking?

Tax advantages may include deductions on property taxes and potential capital gains tax benefits. Consultation with a tax professional is advisable.

Can land banking be done on a smaller scale for individual investors?

Yes, individual investors can engage in land banking on a smaller scale. The key is thorough research and strategic decision-making.

Are there risks specific to land banking that investors should be aware of?

Yes, risks include market fluctuations, environmental concerns, and regulatory changes. Understanding and mitigating these risks are crucial.

Investing in index funds can be a lucrative strategy for building wealth over time, but the key to success lies in understanding the recommended time frame for optimal results. In this article, we’ll delve into the intricacies of index fund investments, exploring the considerations that investors should bear in mind when deciding between short-term and long-term investment horizons.

Time Frame for Index Funds Investing

Understanding Index Funds

Index funds are investment vehicles that aim to replicate the performance of a specific market index, such as the S&P 500. These funds offer a diversified portfolio, typically mirroring the composition of the chosen index. The beauty of index funds lies in their passivity; they don’t rely on active management but rather track the market’s ups and downs.

Recommended Time Frame for Investing

Short-term vs. Long-term Investment Goals

Investors need to define their goals before determining the suitable time frame for investing in index funds. Short-term goals, such as saving for a down payment on a house or funding a vacation, may require a different approach than long-term goals like retirement planning.

Factors Influencing the Time Frame Decision

Several factors influence the decision between short-term and long-term investments. Market conditions, risk tolerance, and individual financial goals all play a role in determining the optimal time frame for investing in index funds.

Short-term Investment Considerations

Market Volatility and its Impact on Short-term Investments

Short-term investments are susceptible to market volatility, which can lead to unpredictable fluctuations in the value of index funds. Investors must be prepared for short-term losses and gains, understanding that market conditions can be highly unpredictable over shorter durations.

Strategies for Short-term Index Fund Investments

To navigate the volatility of short-term investments, investors may consider employing strategies such as setting clear profit targets, using stop-loss orders, and staying informed about market news and events that may impact their holdings.

Long-term Investment Considerations

Benefits of Long-term Investing in Index Funds

While short-term investments may be subject to market turbulence, long-term investments in index funds offer the potential for sustained growth. The power of compound interest becomes a significant advantage over time, allowing investors to capitalize on the overall upward trajectory of the market.

Compound Growth and Wealth Accumulation

Long-term investors benefit from the compounding effect, where returns generate additional returns. This compounding can result in substantial wealth accumulation over an extended period, making index funds an attractive option for those with a patient investment approach.

Long-term investors benefit from the magic of compounding, where their money earns returns on previous gains. By embracing patience and allowing investments to grow over time, investors can harness the full potential of compounding and lay the foundation for a robust financial future.

Regular Contributions and Dollar-Cost Averaging

Consistent contributions to index funds, regardless of market conditions, is a strategy known as dollar-cost averaging. This method involves regularly investing a fixed amount, smoothing out the impact of market volatility. Over time, this disciplined approach can lead to a more stable and predictable investment journey.

Market Trends and Economic Indicators

Analyzing Market Trends for Optimal Investment Decisions

Successful index fund investing requires a keen understanding of market trends. Analyzing historical data and identifying patterns can help investors make informed decisions, aligning their investments with market dynamics.

Key Economic Indicators Affecting Index Fund Performance

Economic indicators, such as interest rates, inflation, and employment figures, can significantly impact index fund performance. Investors should stay informed about these indicators to anticipate potential market movements.

Risk Management in Index Fund Investments

Diversification Strategies

Diversification is a key risk management strategy for index fund investors. By spreading investments across different sectors and asset classes, investors can reduce the impact of poor-performing assets on their overall portfolio.

Understanding and Mitigating Investment Risks

Risk is inherent in any investment, but understanding and mitigating risks are crucial for long-term success. Investors should assess their risk tolerance and make strategic decisions that align with their comfort level and financial objectives.

Perplexity in Investment Decision-making

Addressing the Complexity and Unpredictability of the Market