In this digital age, teaching children about money from an early age is essential. One way to instill financial literacy in your child is through the power of books. We’ve curated a list of top investment books designed specifically for 3-year-olds. These books aim to spark financial curiosity in young minds, laying the foundation for a lifetime of smart financial decision-making.

Top Investment Books for 3-Year-Olds: Sparking Financial Curiosity

Why Start Early?

The Importance of Early Financial Education

Starting financial education at an early age has long-lasting benefits. Children are like sponges, absorbing information and habits quickly. By introducing financial concepts in the form of captivating stories, you can prepare your child for a prosperous financial future.

Building Strong Financial Foundations

A solid understanding of money and investments can empower your child to make informed decisions as they grow older. It’s akin to teaching them a lifelong skill that can help secure their financial well-being.

The Top Investment Books

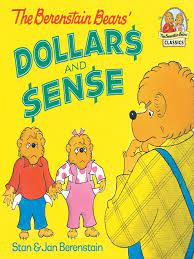

The Berenstain Bears’ Dollars and Sense by Stan and Jan Berenstain

“The Berenstain Bears’ Dollars and Sense” by Stan and Jan Berenstain is a delightful addition to the beloved Berenstain Bears series, known for its ability to impart valuable life lessons in an engaging and accessible way. This book is a fantastic resource for parents looking to introduce their young children to the basics of money, saving, and spending.

In this engaging story, Brother and Sister Bear embark on a financial adventure, learning valuable lessons about the world of money and personal finance. As with many Berenstain Bears books, the characters and their experiences are relatable to kids, making it easier for them to understand and connect with the material.

The narrative is centered around a school project, where the cubs are tasked with managing a small amount of money. The book takes young readers through the ups and downs of spending, saving, and budgeting as Brother and Sister Bear make choices and face the consequences. Through these relatable scenarios, children are introduced to important financial concepts, including the value of saving for future goals.

“The Berenstain Bears’ Dollars and Sense” beautifully weaves financial education into a heartwarming story that emphasizes the importance of wise money management. It encourages kids to think about their spending choices and the impact of those decisions on their savings.

One of the book’s notable features is its charming illustrations, which bring the story to life and engage young readers. The Berenstain Bears series is known for its vivid, colorful artwork, and this book is no exception. The illustrations complement the story, making it even more appealing to children.

Parents can use “The Berenstain Bears’ Dollars and Sense” as a starting point for discussions about money and financial responsibility. It opens the door to essential conversations about saving for goals, making thoughtful spending choices, and understanding the value of money.

In summary, “The Berenstain Bears’ Dollars and Sense” is a fantastic resource for teaching kids about money in a fun and engaging way. It imparts valuable financial wisdom in a manner that is accessible to young children, making it an excellent tool for parents who want to instill early lessons in financial literacy. This book is sure to become a cherished addition to any child’s library, providing not only a good read but also a valuable life lesson.

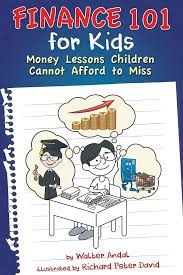

Finance 101 for Kids: Money Lessons Children Cannot Afford to Miss by Walter Andal

Financial literacy is a critical life skill, and it’s never too early to start teaching children about money and personal finance. “Finance 101 for Kids: Money Lessons Children Cannot Afford to Miss” by Walter Andal is a remarkable resource that equips parents and educators with an accessible and engaging way to introduce kids to the world of finance.

This book is not just another addition to the children’s literature on money; it’s a comprehensive guide that takes kids on a journey through fundamental financial concepts. Walter Andal, a seasoned financial expert, skillfully breaks down complex financial ideas into age-appropriate language and relatable scenarios.

One of the book’s strengths lies in its ability to gradually introduce children to money-related concepts, starting with the basics and gradually building up to more complex ideas. From understanding what money is and how it works to explaining the concepts of saving, spending, budgeting, and investing, “Finance 101 for Kids” covers a wide range of financial topics.

The narrative is interactive and engaging, making use of relatable stories and examples that kids can connect with. Andal uses a combination of storytelling and colorful illustrations to bring financial lessons to life, capturing the attention of young readers and making the concepts easy to comprehend.

What truly sets this book apart is its practical approach to financial education. It doesn’t just tell children about money; it encourages them to apply what they’ve learned through fun exercises and activities. This hands-on aspect of the book empowers kids to put their newfound knowledge into practice, reinforcing the lessons in a meaningful way.

“Finance 101 for Kids” serves as a valuable resource for both parents and teachers who aim to instill important money lessons in children. It offers a comprehensive and engaging foundation in financial literacy, ensuring that children are well-prepared to navigate their financial journey as they grow.

In a world where financial decisions play a significant role in our lives, teaching kids about money is an investment in their future. Walter Andal’s book is a beacon in this quest, offering money lessons that children cannot afford to miss. It’s a must-have for any child’s library, equipping them with the knowledge and skills to make sound financial choices throughout their lives.

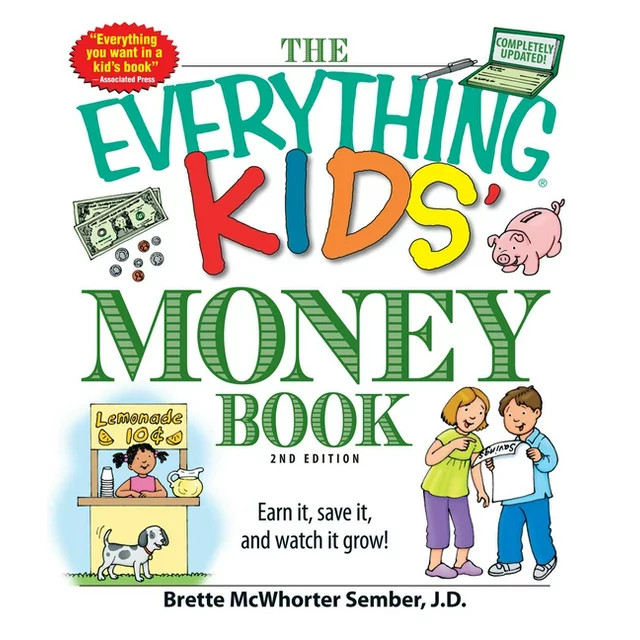

The Everything Kids’ Money Book: Earn it, save it, and watch it grow! by Brette Sember

. “The Everything Kids’ Money Book: Earn it, save it, and watch it grow!” by Brette Sember is a remarkable resource that empowers young minds with practical and engaging financial knowledge.

This book is not just another children’s book about money; it’s a comprehensive guide that demystifies financial concepts for kids in a way that is easy to understand and relatable. Brette Sember, an experienced writer and expert in family and finance matters, has crafted a resource that takes kids on a journey from the basics of money to more complex financial ideas.

The strength of “The Everything Kids’ Money Book” lies in its ability to break down seemingly complex concepts into digestible pieces. It starts with the fundamental principles of what money is, how it is earned, and why it is important. As the book progresses, it delves into topics like budgeting, saving, investing, and even understanding financial institutions, making it a comprehensive guide to financial literacy for children.

One of the book’s notable features is its interactive approach to teaching finance. It encourages kids to apply what they’ve learned through hands-on activities, quizzes, and exercises. This not only reinforces the lessons but also makes learning about money enjoyable.

The language used in the book is child-friendly and engaging, making it accessible to young readers. It avoids jargon and complicated terminology, ensuring that kids can easily grasp the concepts being presented. The book is further enhanced by colorful illustrations and a vibrant layout, making it visually appealing to children.

“The Everything Kids’ Money Book” is a fantastic resource for parents, teachers, and caregivers who want to equip children with essential financial knowledge. It goes beyond just explaining the principles of money; it encourages practical application, empowering kids to take control of their financial future.

If you Made a Million by David M. Schwartz

“If You Made a Million” by David M. Schwartz is a delightful and educational book that takes young readers on a financial adventure, making complex money-related concepts accessible and engaging.

The book is essentially a journey of discovery, narrated by two young siblings, Marcy and Jake, who embark on a quest to learn about the world of finance. Through colorful and imaginative illustrations, readers are introduced to various financial concepts, such as earning, saving, spending, and investing, in a way that is both fun and relatable.

David M. Schwartz uses clever scenarios and comparisons to explain complex ideas. For instance, he likens the concept of a million dollars to stacks of $1,000 bills, helping children visualize the sheer magnitude of such a sum. This approach is not only informative but also captivating for young minds.

One of the book’s key strengths is its interactivity. Throughout the story, readers are encouraged to actively participate by solving financial puzzles, calculating interest, and understanding the difference between income and expenses. This hands-on approach makes the learning experience dynamic and engaging.

The language used in “If You Made a Million” is accessible to children, avoiding overly technical terms and explanations. The narrative is supplemented by vivid and whimsical illustrations by Steven Kellogg, which add a layer of charm to the book and help bring the financial concepts to life.

The book’s emphasis on the practical application of financial knowledge is another notable feature. It inspires children to consider the financial choices they make and encourages them to think about how they can use their money wisely. Through this journey of discovery, kids not only learn about money but also gain a sense of financial responsibility.

The Four Money Bears by Mac Gardner

The Four Money Bears is a financial literacy book for kids written by Mac Gardner. It tells the story of four bears, each of whom represents a different way to manage money:

- Spender Bear: Spender Bear loves to spend money. He buys everything he sees, even if he doesn’t need it.

- Saver Bear: Saver Bear loves to save money. He puts away money every month and invests it so that it can grow over time.

- Investor Bear: Investor Bear loves to invest money. He buys stocks, bonds, and other investments in the hope of making money in the future.

- Giver Bear: Giver Bear loves to give money to charity. He believes in helping others and making the world a better place.

The Four Money Bears learn that there is no one right way to manage money. The best way to manage money is to find a balance between spending, saving, investing, and giving.

The Four Money Bears is a great book to teach kids about the basics of financial literacy. It is written in a simple and engaging way, and the illustrations are colorful and fun. The book also includes a few activities at the end to help kids practice what they have learned.

Here are a few key takeaways from the book:

- It is important to have a plan for your money.

- It is important to save money for the future.

- It is important to invest money so that it can grow over time.

- It is important to give back to the community.

The Four Money Bears is a great book for parents and teachers to read to their children. It is a fun and educational way to teach kids about financial literacy.

How to Make Reading Fun

Engaging Activities

Make the learning experience more enjoyable by engaging your child in activities related to the stories. Create a “savings jar” where they can keep their coins or play a game where they make financial decisions.

Reading Together

Reading these books together not only strengthens the parent-child bond but also allows you to explain financial concepts as you go along, ensuring that they understand the material.

Conclusion

Teaching financial literacy to 3-year-olds might sound challenging, but with the right books, it can be a delightful experience. The top investment books mentioned above are powerful tools to spark your child’s financial curiosity. By instilling these concepts early on, you are setting the stage for a financially savvy future.

FAQs

FAQ 1: When is the right time to start teaching kids about money?

The earlier, the better! 3-year-olds are curious and eager learners, making it an ideal age to introduce basic financial concepts.

FAQ 2: How can I make financial education fun for my child?

Use interactive activities, games, and engaging books to make the learning process enjoyable and relatable.

FAQ 3: Are these books suitable for older kids too?

While these books are designed for 3-year-olds, they can be a great introduction for older children as well. For older kids, you can explore more advanced financial books.

FAQ 4: Can these books really make a difference in my child’s financial future?

Yes, they can! By introducing financial concepts at an early age, you’re giving your child a head start in understanding money, investments, and making wise financial choices.

FAQ 5: Where can I find these books?

You can find these books in local bookstores, libraries, or online retailers. Additionally, some are available as e-books for convenient access on digital devices.